![]()

Key Takeaways

- Business tax write-offs that reduce taxable income can significantly hurt conventional mortgage approval chances for self-employed borrowers

- Alternative loan products like bank statement loans and DSCR loans focus on actual cash flow rather than adjusted gross income from tax returns

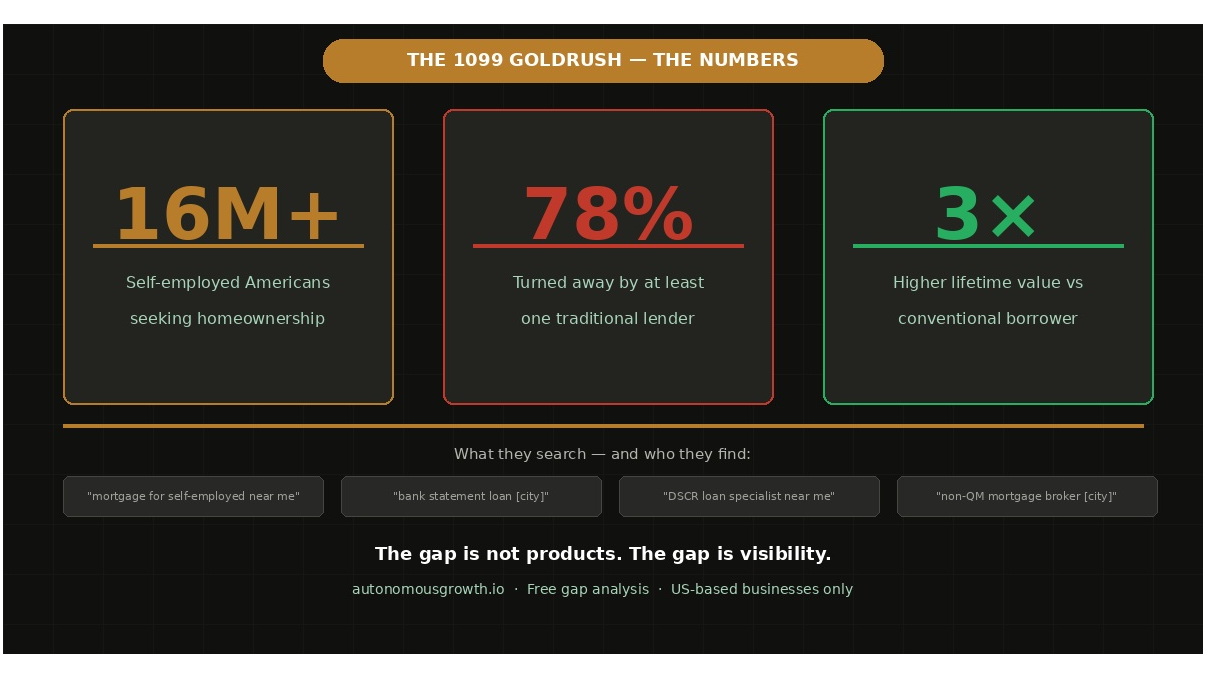

- Over 16 million self-employed Americans face unique mortgage challenges that traditional lenders often misunderstand

- Non-QM lenders specialize in complex income situations that don’t fit conventional lending criteria

- Strategic documentation beyond tax returns can unlock homeownership opportunities for business owners and contractors

Self-employed professionals across America face a frustrating paradox: the same tax strategies that keep their businesses financially healthy are the exact reasons mortgage lenders reject their applications. Smart business owners maximize deductions to minimize tax liability, but this approach creates a paper trail that makes their actual earning power invisible to conventional mortgage underwriters.

Your Business Write-Offs Are Hurting Your Home-Buying Chances

Every legitimate business expense deduction tells a story of financial responsibility and operational efficiency. Vehicle expenses, home office deductions, equipment purchases, travel costs, and professional services all represent real business investments that reduce taxable income. However, mortgage lenders see these deductions very differently than business owners do.

A freelance consultant who writes off $15,000 in legitimate business expenses sees their tax liability decrease substantially. Their actual cash flow might support a $3,000 monthly mortgage payment comfortably, but their tax return shows an adjusted gross income that barely qualifies them for a $1,500 payment. Autonomous Growth works with mortgage professionals who understand this disconnect affects millions of qualified borrowers every year.

The tax code encourages business owners to deduct legitimate expenses, while mortgage qualification guidelines essentially penalize them for following good business practices. This fundamental mismatch explains why so many successful entrepreneurs struggle with conventional mortgage approval despite having strong cash flow and substantial assets.

Why Lenders Reject Strong Self-Employed Borrowers

Adjusted Gross Income vs. Actual Cash Flow

Traditional mortgage underwriting relies heavily on adjusted gross income from tax returns, which represents income after all deductions have been applied. A business owner grossing $120,000 annually might show only $65,000 in adjusted gross income after legitimate business deductions. Lenders calculate debt-to-income ratios using that lower figure, even though the borrower’s actual spending power more closely reflects their gross business income.

Cash flow analysis tells a completely different story than tax return analysis. Bank statements reveal consistent deposits, operational expenses, and net cash available for personal use. Many self-employed borrowers maintain strong positive cash flow month after month, despite showing relatively modest adjusted gross income on their tax returns.

The Two-Year Income History Trap

Conventional mortgage guidelines require two years of tax returns to establish income stability for self-employed borrowers. This requirement assumes that past performance predicts future earning capacity, but entrepreneurial income often follows different patterns than traditional employment income.

New business owners who transitioned from W-2 employment face particular challenges. A successful consultant who left corporate employment to start their own practice might earn significantly more as an independent contractor, but they lack the two-year self-employment history that conventional lenders require. Their W-2 income history doesn’t reflect their current earning potential, and their new business income appears too brief to establish a pattern.

Debt-to-Income Ratios That Don’t Tell the Story

Standard debt-to-income calculations fail to account for the financial flexibility that many self-employed borrowers actually possess. Business owners can often adjust their income timing, accelerate or defer certain expenses, and manage cash flow in ways that W-2 employees cannot.

A restaurant owner might show seasonal income fluctuations that concern traditional underwriters, but their annual cash flow remains strong and predictable. Their ability to manage business expenses, adjust operating costs, and generate additional revenue streams provides financial stability that standard debt-to-income ratios don’t capture.

Alternative Mortgage Solutions That Actually Work

1. Bank Statement Loans – Prove Cash Flow Without Tax Returns

Bank statement loans allow borrowers to qualify using 12 to 24 months of personal or business bank statements instead of tax returns. Lenders analyze deposit patterns, average monthly income, and cash flow consistency to determine qualification. This approach reveals the borrower’s true earning capacity rather than their tax-minimized adjusted gross income.

Most bank statement loan programs calculate qualifying income by averaging total deposits and subtracting an estimated expense ratio. These ratios typically range from 10% to 75% depending on the business type and lender requirements. A freelance graphic designer showing $8,000 in monthly deposits might qualify based on $6,000 in monthly income using a 25% expense ratio, regardless of what their tax returns show.

2. DSCR Loans – Property Income Matters More Than Personal Income

Debt Service Coverage Ratio loans focus entirely on the rental income potential of investment properties rather than the borrower’s personal income documentation. These loans calculate whether the property’s rental income can cover the mortgage payment, with ratios typically ranging from 1.0 to 1.25 times the monthly payment amount.

Real estate investors use DSCR loans to acquire rental properties without providing personal tax returns or employment verification. The property’s rent roll, lease agreements, and market rent analysis determine qualification. A duplex generating $3,000 in monthly rental income can support a mortgage payment of $2,400 using a 1.25 DSCR ratio.

3. Profit & Loss Loans – CPA Documentation Opens Doors

Profit and loss statement loans accept CPA-prepared financial statements in place of tax returns for income verification. These programs work particularly well for borrowers whose businesses generate strong cash flow but minimize taxable income through strategic deductions and depreciation.

A CPA-prepared profit and loss statement can present a more accurate picture of business performance than tax returns alone. Business owners can work with their accountant to prepare statements that reflect operational income before certain tax-motivated deductions, providing lenders with a clearer view of actual earning capacity.

4. Asset Depletion Programs – Net Worth Speaks Louder

Asset depletion programs calculate qualifying income by dividing the borrower’s liquid assets by a specific number of months. While 360 months (30 years) is commonly used, lenders may also use 180 months (15 years) or other terms depending on the program and borrower situation. Borrowers with substantial investment accounts, retirement savings, or business assets can qualify based on their net worth rather than documented income flow.

A semi-retired business owner with $2 million in investment accounts might qualify for significant mortgage amounts using asset depletion calculations, even if their current income documentation appears modest. These programs work especially well for borrowers transitioning between career phases or managing wealth rather than actively earning traditional income.

1099 Contractors Face Unique Mortgage Challenges

Income Consistency Requirements

Independent contractors receiving 1099 income often experience seasonal fluctuations or project-based earnings that don’t align with traditional employment patterns. Lenders struggle to evaluate income that varies significantly from month to month, even when annual totals remain strong and predictable.

Many 1099 contractors work with multiple clients, creating diverse income streams that provide stability through diversification. However, mortgage underwriters often view multiple income sources as increased risk rather than decreased risk, preferring the apparent simplicity of single-employer W-2 income.

Required Documentation Beyond Tax Forms

Lenders typically require 1099 contractors to provide additional documentation beyond standard tax returns. Profit and loss statements, bank statements, contracts with major clients, and sometimes even client reference letters become necessary to paint a complete picture of income stability and future earning potential.

Some lenders require evidence of business licensing, professional certifications, or industry credentials that support the contractor’s ability to maintain consistent income. This documentation helps underwriters understand the borrower’s market position and competitive advantages within their industry.

Finding Specialists Who Understand Your Situation

Non-QM Lenders vs. Traditional Banks

Non-Qualified Mortgage lenders specialize in complex income situations that don’t fit conventional lending guidelines. These lenders understand business cash flow analysis, alternative income documentation, and the financial patterns of self-employed borrowers. They often employ underwriters with business ownership experience who can evaluate entrepreneurial income more accurately.

Traditional banks typically focus on conventional loan products with standardized underwriting criteria. While some major banks offer alternative documentation programs, their underwriters may lack the specialized knowledge needed to properly evaluate complex business income situations.

Questions to Ask Potential Loan Officers

Self-employed borrowers should ask specific questions to identify loan officers with relevant expertise. Key questions include: “What percentage of your business involves self-employed borrowers?”, “Which alternative documentation programs do you offer?”, and “Can you walk me through how you calculate qualifying income from bank statements?”

Experienced non-QM loan officers can explain multiple qualification strategies and help borrowers choose the documentation approach that best presents their financial situation. They should be able to discuss the pros and cons of different loan products and provide realistic expectations about rates, terms, and qualification requirements.

Over 16 Million Self-Employed Workers Need Better Mortgage Access

The self-employed workforce continues growing as more professionals choose entrepreneurship, freelancing, and independent contracting over traditional employment. This demographic shift creates an expanding pool of potential homebuyers who don’t fit conventional mortgage qualification criteria but possess genuine ability to repay mortgage debt.

Market research indicates that self-employed borrowers often become loyal clients who refer other entrepreneurs and business owners to loan officers who successfully help them achieve homeownership. Building expertise in alternative documentation and non-QM lending creates opportunities to serve an underserved but growing market segment.

Current mortgage industry practices leave millions of qualified borrowers without adequate financing options, creating opportunities for lenders who develop specialized knowledge and processes for evaluating entrepreneurial income. As the gig economy and remote work trends continue expanding, the demand for flexible mortgage qualification approaches will likely increase substantially.

Autonomous Growth helps mortgage professionals build digital authority and capture leads from self-employed borrowers actively searching for specialists who understand their unique financial situations.

Autonomous Growth ( part of RReputatioNN )

109 Sint-Lenaartsesteenweg #1

1

Rijkevorsel

Antwerpen

2310

Belgium